There’s no denying Ireland has a strong economy. But it has a strange economy. Ireland depends to an extraordinary extent on investment from elsewhere.

Foreign investment is no bad thing. It has brought jobs and raised living standards. But it comes with problems. It absorbs talent and other resources. It leaves Ireland dependent on factors, such as US tax law, that are beyond its control.

Ireland has ambitions to be more than a car park for American technology and pharmaceutical companies. It wants to diversify its industrial base. It wants to be a minor global capital of technological innovation.

But Ireland is making it hard for its own technology industry. Ireland’s tax setup — the one that has attracted so much investment from foreign companies — is a severe drag on domestic companies.

Imagine two identical entrepreneurs. One is from Ireland, the other is from somewhere in the EU. They both have identical business ideas. They both need €1 million in funding. After five years, they both forecast their investors will get back €11.3 million. They both take their idea to a venture capital investor who’s targeting 30 per cent returns.

What you’d expect to happen is that the European entrepreneur would get funded, but the Irish entrepreneur would not. The Irish entrepreneur wouldn’t expect to get funded because higher Irish taxes would make the investment unviable. To make up for higher Irish taxes, the Irish company would need to make €23.7 million for investors after five years. That’s a much taller order than €11.3 million. More on this calculation later.

Irish entrepreneurs need to be smarter, harder working, or luckier than Europeans to achieve the same results.

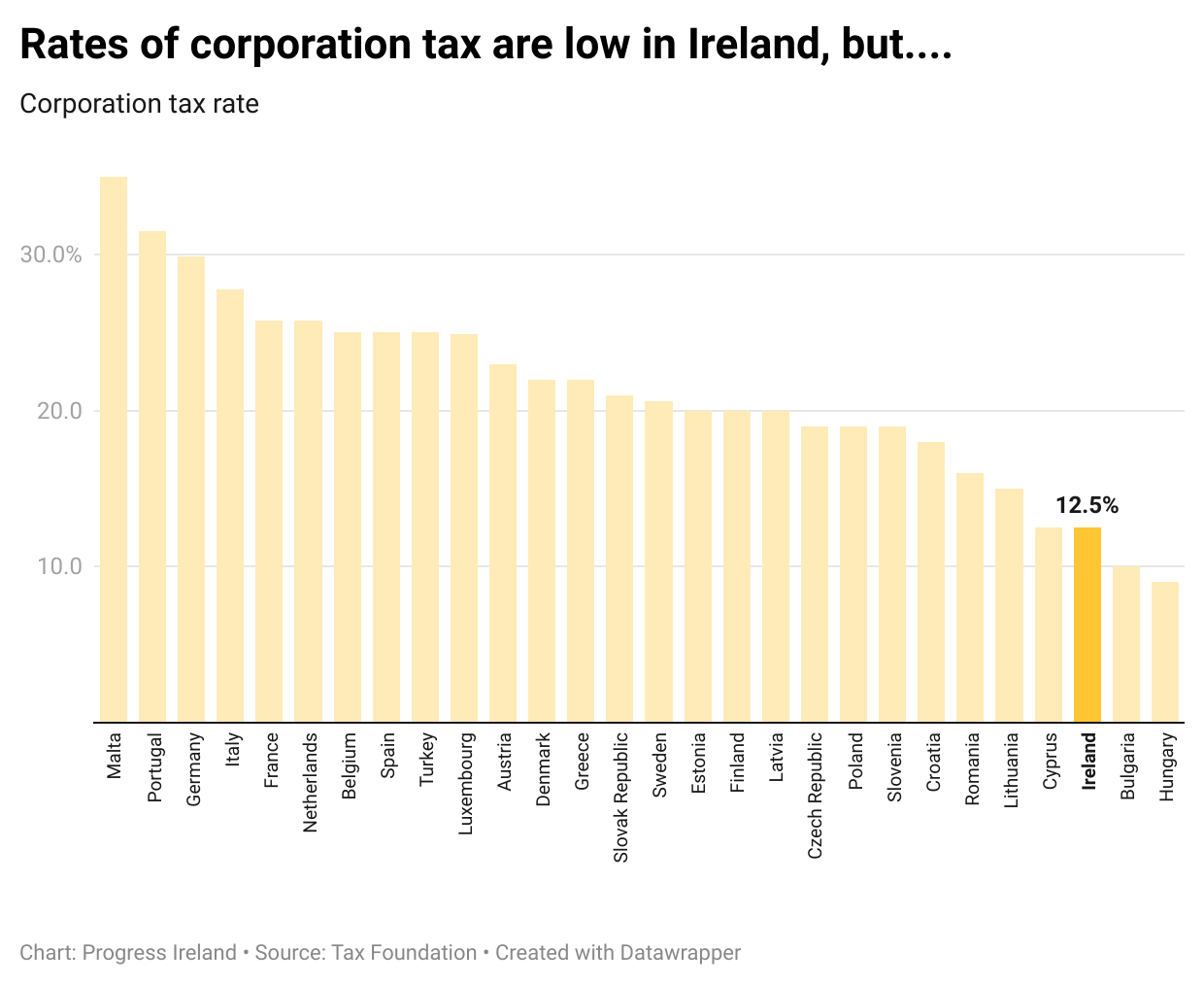

Ireland taxes foreign and domestic companies differently

Ireland is known for having low corporation taxes. But corporation taxes are only one of three main ways investors are taxed.

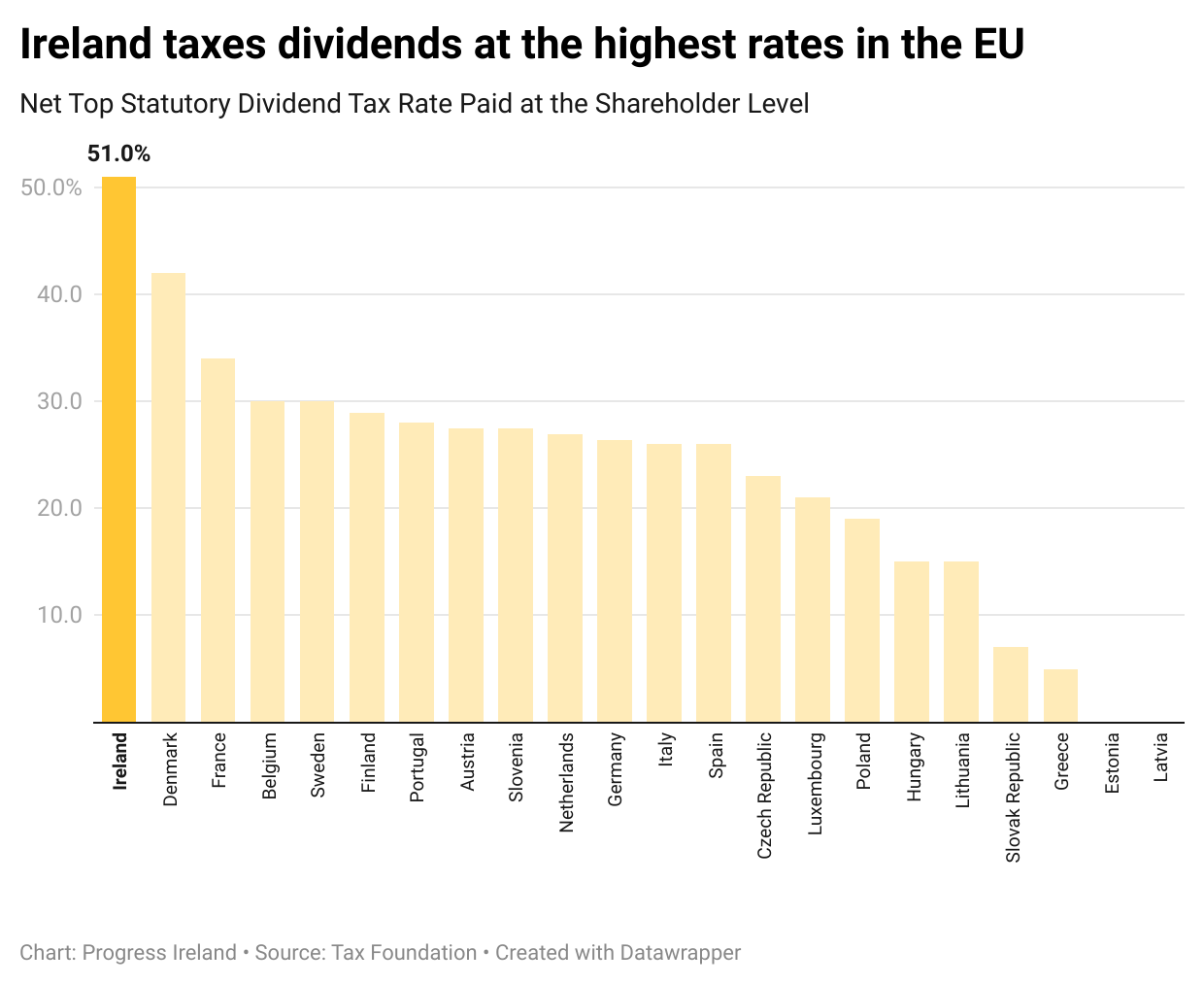

The next important tax on investors is the tax on dividends. This tax is levied on money transferred from the company to its owners. Irish dividend taxes are the highest in the EU.

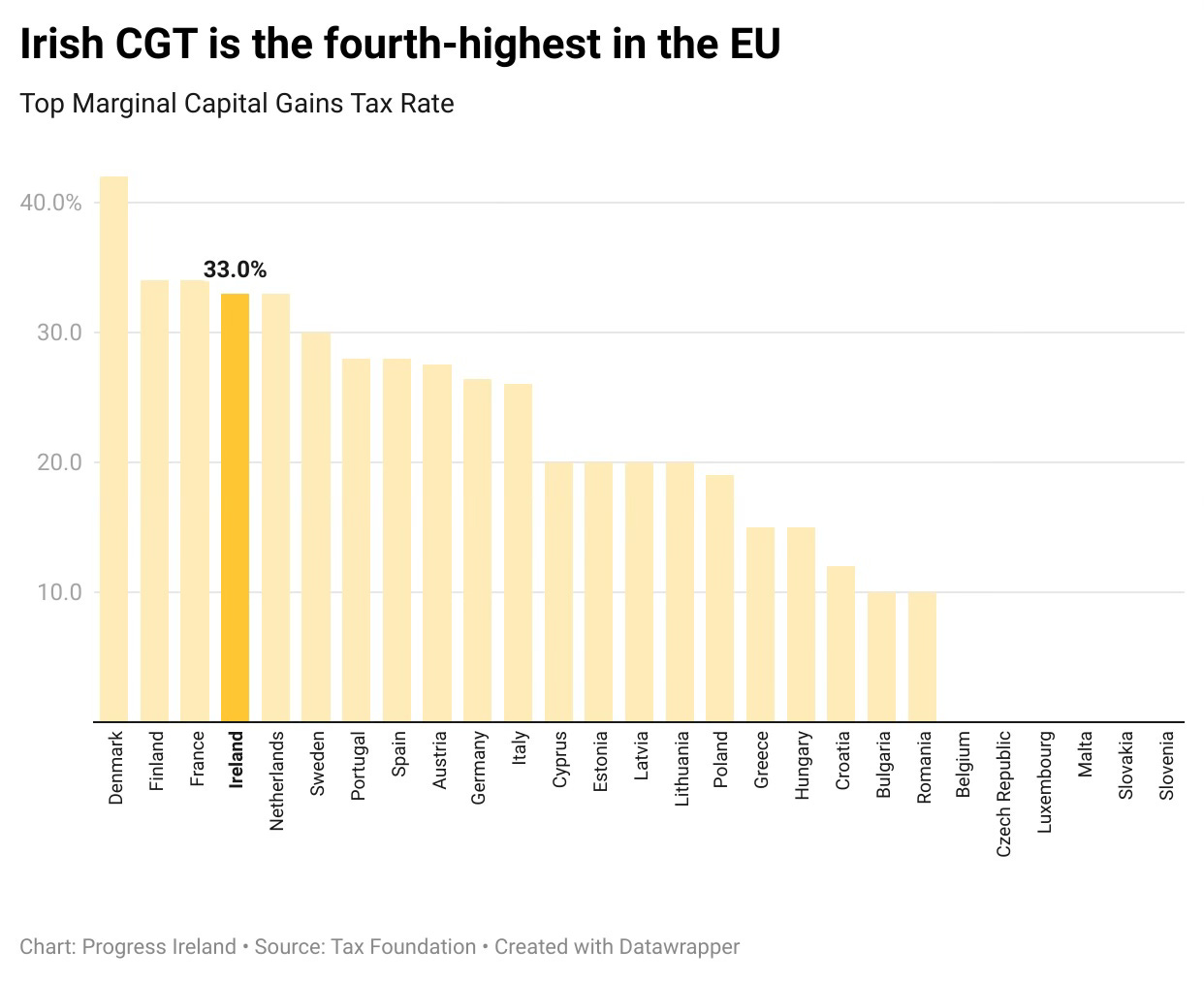

The last big tax on investors is on capital gains (CGT). This is a tax on the profit earned when an asset is sold for more than it was paid for. If an investor sells shares in a company at a profit, they must pay CGT. Irish CGT is the fourth-highest in the EU.

Low corporation taxes are good for foreign investors. They get to base their business in Ireland where profits are taxed lightly, then return the proceeds to the mothership where they can be passed on to investors.

Investors in Irish companies don’t have that option. To take money out of an Irish business, the investor must pay a dividend tax rate of 52 per cent, which as we’ve seen is the highest in the EU and twice the EU average. If the investor tries to realise the value of the business by selling shares, they must pay capital gains tax of 30 per cent, the fourth-highest in the EU. Irish companies are may be lightly, but investors in Irish companies are not.

To be sure, all investors don’t pay the statutory tax rate. Tax law is complicated in every country. There are many carve-outs and exemptions. The calculations below are based on the statutory tax rate, not the effective rate.

Hurdlers

I said a hypothetical Irish entrepreneur would need to generate a €23.7 million payout after five years to get funded, compared to €11.3 million in Europe. How did I get those numbers?

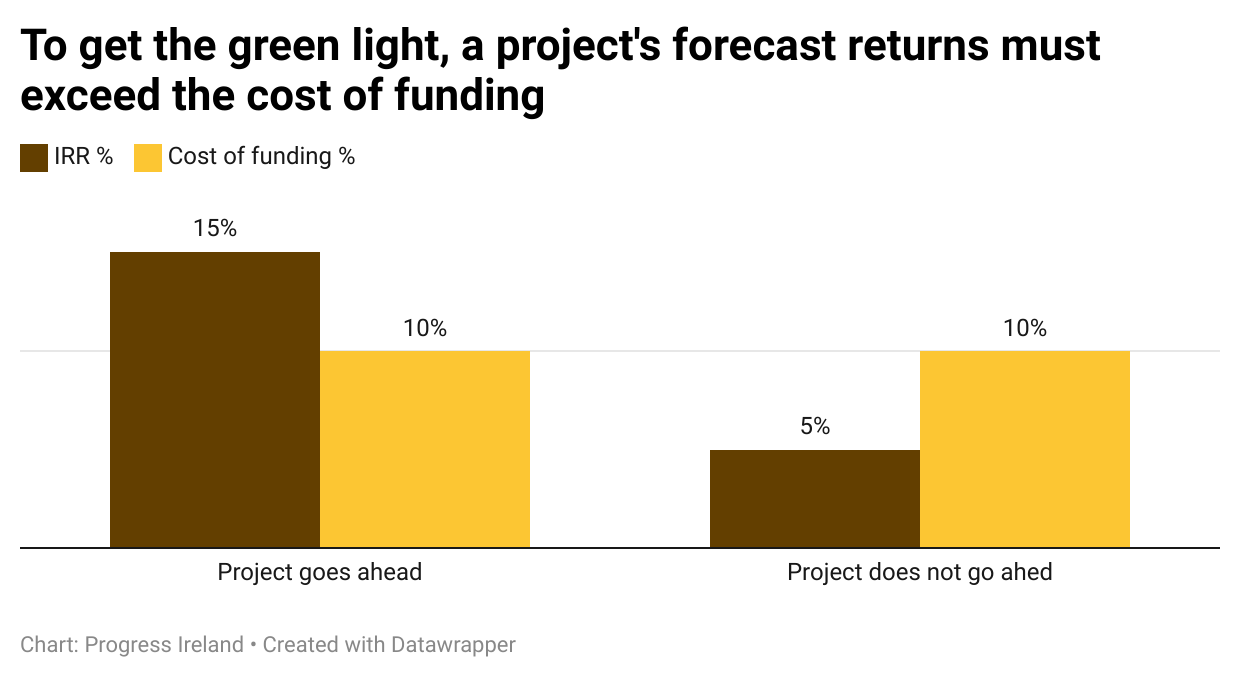

It comes from the idea of a hurdle rate. When deciding whether a project should go ahead, there are two relevant numbers: the project’s expected return and the cost of funding. If the expected return is higher than the cost of funding, the project can go ahead. The cost of funding is the hurdle the expected return must surmount. For a five year VC funded project, and initial investment of €1 million, the pre-tax hurdle rate for the average EU firm is €11.3 million. For an Irish firm it’s €23.7 million.

There are different ways to calculate expected return, but they’re basically about the amount of money the project will bring in over time, after tax. The more the better. This is expressed as an annualised number.

The cost of funding is slightly more complicated. Again, it’s expressed as an annualised number – a rate of return per year. The number varies depending on the source of the funding. Funding can either come from debt; shares (AKA equity); or a mixture of both.

For a project that’s funded entirely by debt, the cost of funding would simply be the after-tax interest rate.

The most exciting technology projects, however, aren’t funded by debt. They’re funded entirely by equity. The funding for tech startups usually comes from a specialised investor called a venture capitalist, or VC. VC-backed projects are particularly important to Ireland because they’re the high-tech, high value added businesses on which our future economy will depend.

If the interest rates is the cost of debt funding, what’s the cost of equity funding ? It’s the annual rate of return on an equity investment. It basically means “what’s the minimum after-tax return an investor expects to make per year to compensate for the risk of backing this project”.

An effort to model how all these taxes impact Irish investors

What we’re interested in is the tax component of this. Taxes get between companies and their funders. Taxes on dividends, profits and capital gains drag down after tax returns, which means they push up the pre tax profit a company needs to make in order to justify an investment.

Taxes impact companies at different stages of their life cycle. How do taxes change the hurdle rates for startups?

What follows is an effort to model the impact of the three most important taxes on hurdle rates, based on some simple assumptions. The assumptions are that investors in young, fast-growing companies seek 30 per cent returns. These young companies are assumed to return no dividends and make no profits. When they mature, companies are assumed to return half their capital in the form of dividends and half as capital gains.

There are two steps to this calculation. The first step is to model the impact of taxes on the value of mature companies. This is because a startup will eventually be valued as a mature company. Taxes impact mature companies differently to young companies, because mature companies pay out more dividends and make more profits.

Investors in startups don’t pay taxes on dividends. But they will eventually sell their shares, and the value of those shares will be impacted by expected future dividend taxes, which will in turn reduce their returns.

VCs’ tax burden is as follows. They pay capital gains taxes when they sell shares for a profit. And the value of the shares they sell is depressed by the expectation of future dividend and corporation taxes.

As we’ve seen, VCs typically expect around 30 per cent annual return after tax if they’re to invest in a risky startup. What would a startup have to generate before tax to hit that number?

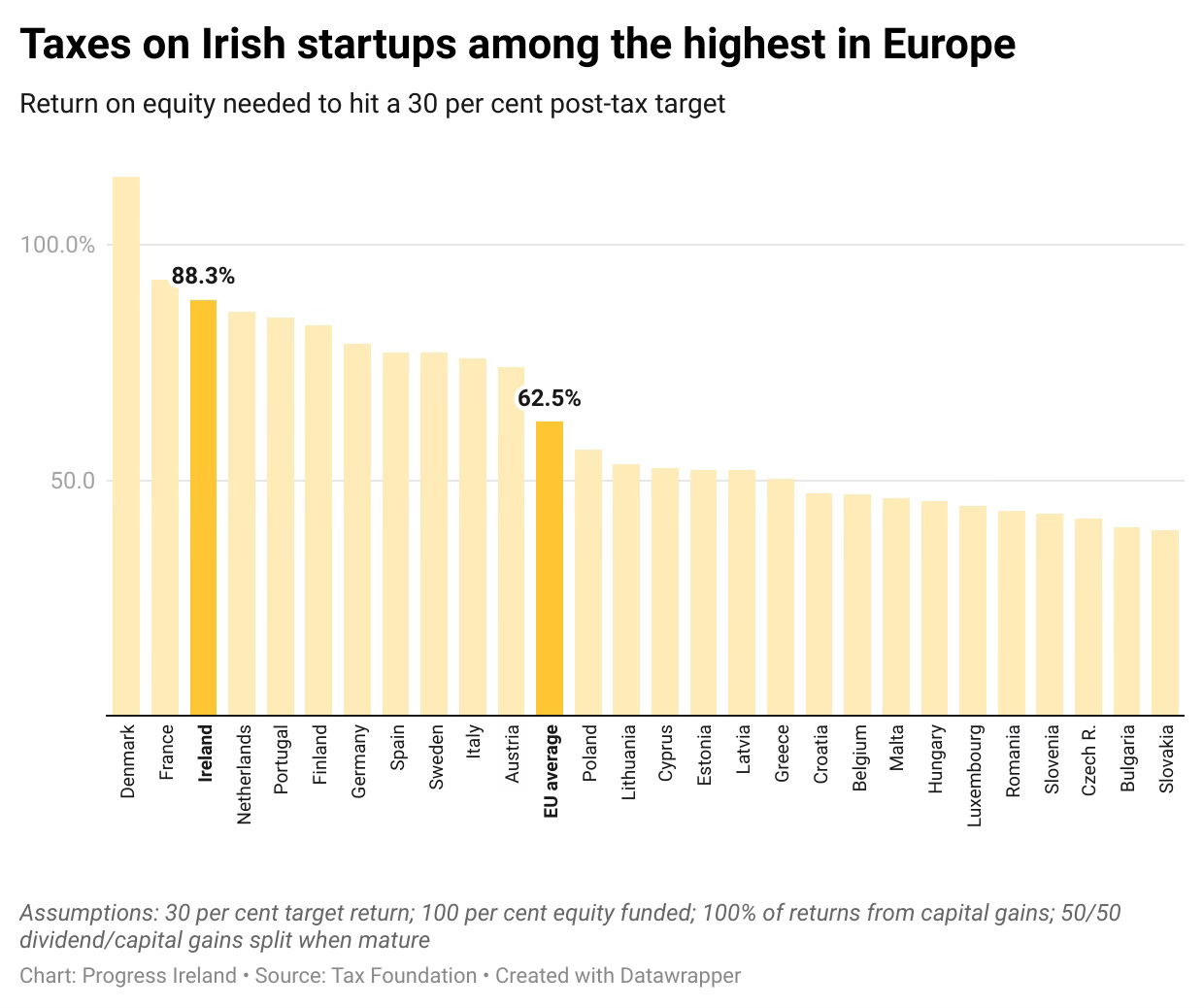

The chart below shows the returns a company would need to achieve a post-tax 30 per cent return in different European countries. We can see that a) all across Europe, taxes on companies drive a big wedge between investors and companies and b) Irish taxes on venture-backed companies are the third-highest in Europe.

The chart above shows Irish firms need an 88.3 per cent pre tax return on equity to meet investor expectations. I said earlier that an Irish startup with €1 million in VC funding would need to return €23.7 million after five years, compared to €11.3 million for an average European startup. How did I get €23.7 million? This figure is based on an internal rate of return (IRR, a profit metric) of 88.3 per cent and a five year time horizon.

To be sure, Irish entrepreneurs are not likely to be running these calculations. They’re coming up with ideas and doing their best to make them happen. Neither are funders precisely calculating startups’ IRRs and comparing it to a 88.3 per cent cost of equity. What happens instead is that successful Irish VCs know they need to be a bit tighter, a bit less flathiúlach, than successful VCs in other countries.

This is the mechanism by which taxes stop projects from going ahead. Projects that investors would like to back, in the absence of taxes, don’t get backed. Software engineers take a job at Google instead of trying their luck. Biotech ideas never reach the lab. Entrepreneurs try their luck in other countries instead.

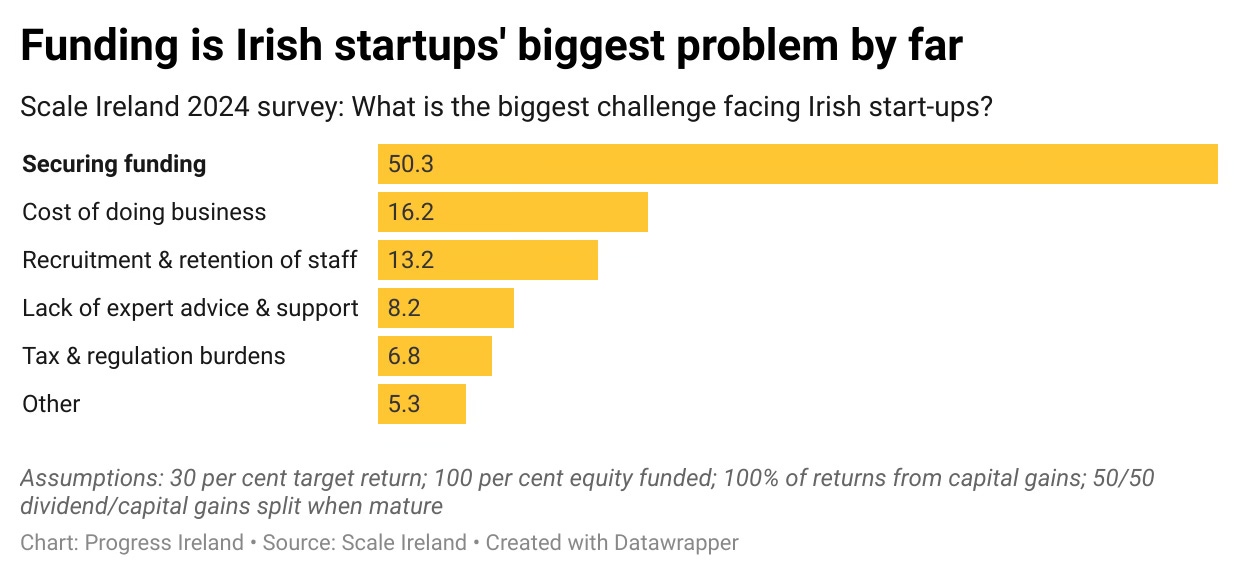

And this is not a trivial problem. Irish startups consistently cite access to funding as their biggest bottleneck.

The purpose of a firm

The social benefits of companies are large. Companies make useful things and they pay wages and taxes. A flourishing Ireland would have lots of world-class Irish companies.

But none of this is the concern of the individual entrepreneur or investor. For them, the only purpose of a company is to return money to its owners. A company that can’t return capital to its owners is failing on its own terms.

It’s a question of priorities. If Ireland is happy to continue to rely on investment from US companies, the tax system is working well.

If it wants Irish companies to provide a counterweight to American ones, it should make some changes.