Muireann Lynch on the surprising strengths, and obvious weaknesses, of our electricity system

When I get stuck on something to do with electricity, Muireann Lynch is the person I call.

Muireann is an economist with the ESRI. Her work is mainly focused on electricity markets.

Muireann has the right toolkit for understanding electricity because electricity is a system with lots of overlapping goals and actors. When something about the system changes, what follows is a complex interaction between many factors, the outcome of which can be hard to forecast. Modelling these dynamic systems like these are an economist’s speciality.

I wanted to interview Muireann for the substack because she always has surprising and counterintuitive things to say about what’s going on with electricity. The first part of the interview is about Ireland’s system. We talk about the surprising strengths and some weaknesses of Ireland’s system. The second section discusses how economists think about electricity.

Ireland’s energy system

Seán Keyes: What are the strengths and weaknesses of the energy system we’re building?

Muireann Lynch: I think we have an incredibly reliable power system. We have a super-sophisticated suite of what we call system services. These are essentially products to make sure the power system is very nimble, able to respond very close to real time disturbances. A lot of this is because Ireland has just had to do it, because we’re small.

To a first-order approximation, a disturbance on a very large interconnected power system has a smaller proportional impact on the supply-demand imbalance — and therefore on the stability of the system — than on a small system. So, for example, the cascading failure and the blackouts we saw in Spain and Portugal last year would not have happened in Ireland — even though you’d think they’d be more likely here, because the Irish system is so much smaller and far more vulnerable to the kind of shocks that cause that cascading failure. In terms of what we’re doing right, we’re world leaders on that particular side of things, these reliability metrics and reliability products, and it’s something we don’t get enough credit for, because everyone just says Ireland’s useless at everything.

What are we getting wrong? A number of things. There’s a narrative that the problems are very high-level. For example, I’ve spoken to some people who think the answer to all our problems is that we need a state-owned renewable electricity company that will invest in offshore wind and bring prices down. And I know other people who think the problem is explicitly the Climate Act and our net-zero ambitions. These two narratives come from opposite ends of the spectrum, and they’re both, unfortunately, very misguided.

Our problems are not that fundamental. The devil really is in the details.

First of all, we already have a state-owned company, ESB Power Generation, which owns an awful lot of renewable electricity. They weren’t competitive in some of the renewable electricity auctions. And we have another state-owned company, Bord na Móna, which is essentially a renewable company. Apart from a tiny peaker that runs on gas, pretty much their entire portfolio is renewable electricity.1 So we already have state-owned renewable electricity companies. Setting up another one will not fix anything.

Similarly, is our Climate Act realistic? No. Are we going to hit net zero by 2050? No. But you could repeal that Act tomorrow, and what else would change? Nothing.

Seán Keyes: Why would nothing else change? That implies that removing the goal of sustainability wouldn’t change what we would do, how we would invest.

Muireann Lynch: Well, if you’re not going to meet a goal, then removing a goal you’re not going to meet, by definition, can’t make a difference.

But secondly, we don’t generate enough power — that’s just a fact. We had to procure emergency diesel generators because we don’t have enough investment in the system. We’ve had no investment whatsoever in gas for over a decade, which we really, really need. The only investment we’ve had at all is on the renewable side, and some batteries — and we don’t have enough of that either.

We’re simply not building enough generation of any type to meet our demand, and that’s causing our prices to be higher than they need to be. The idea that what little generation we have been building is somehow part of the problem, purely because it happens to be renewable, is just not in touch with reality.

So, again — to give examples from both sides of the spectrum — the idea that our problem comes down to renewable electricity, whether it’s that we don’t have enough of it, or we have too much of it, or it’s owned by the wrong person, is a dastardly simplistic answer to what is a very complicated question.

What you need to do is look at the details. I think our renewable electricity auctions are badly designed. I think our conventional electricity auctions are badly designed. And the fact that we had about 700 megawatts of conventional generation that won contracts and didn’t show up is a huge problem — one we had to solve by procuring diesel generators. You can have all the Climate Acts, or Climate Act repeals, you like; none of that will affect the details of the T-4 capacity auction.2

Seán Keyes: If the price of wind — deepwater offshore, offshore, onshore — doesn’t drop, what does that do for our plans for the next ten years? Are our plans based on assumptions of lower renewable prices than we’re getting currently?

Muireann Lynch: Not really, no. There were assumptions about what renewable penetration would do to electricity prices — the assumption is that it’ll depress prices, and that’s true; when you do ex-post analysis, for every gigawatt of renewable capacity you see a significant suppression of wholesale prices.

But there’s an inflection point where eventually the wholesale prices are so suppressed that the subsidies required to make wind wash its face cancel out that benefit. We’re not at that inflection point yet. But will we hit it before 80 per cent RES-E (renewable electricity sources)?3 Yes, we will.

Seán Keyes: Where is that inflection point?

Muireann Lynch: It totally depends on the gas price. If gas prices are low, that inflection point comes pretty soon. If gas prices remain at the levels we’ve seen, it could be really high — because the gas price determines the wholesale price.

But the main thing is — and I can tell you this hand on heart, I’ve spoken with the people doing the actual modelling, and procuring the modelling — absolutely nobody is only looking at the price-suppression side of the equation. Everybody is looking at the price-suppression side and the subsidy side, and finding the inflection point.

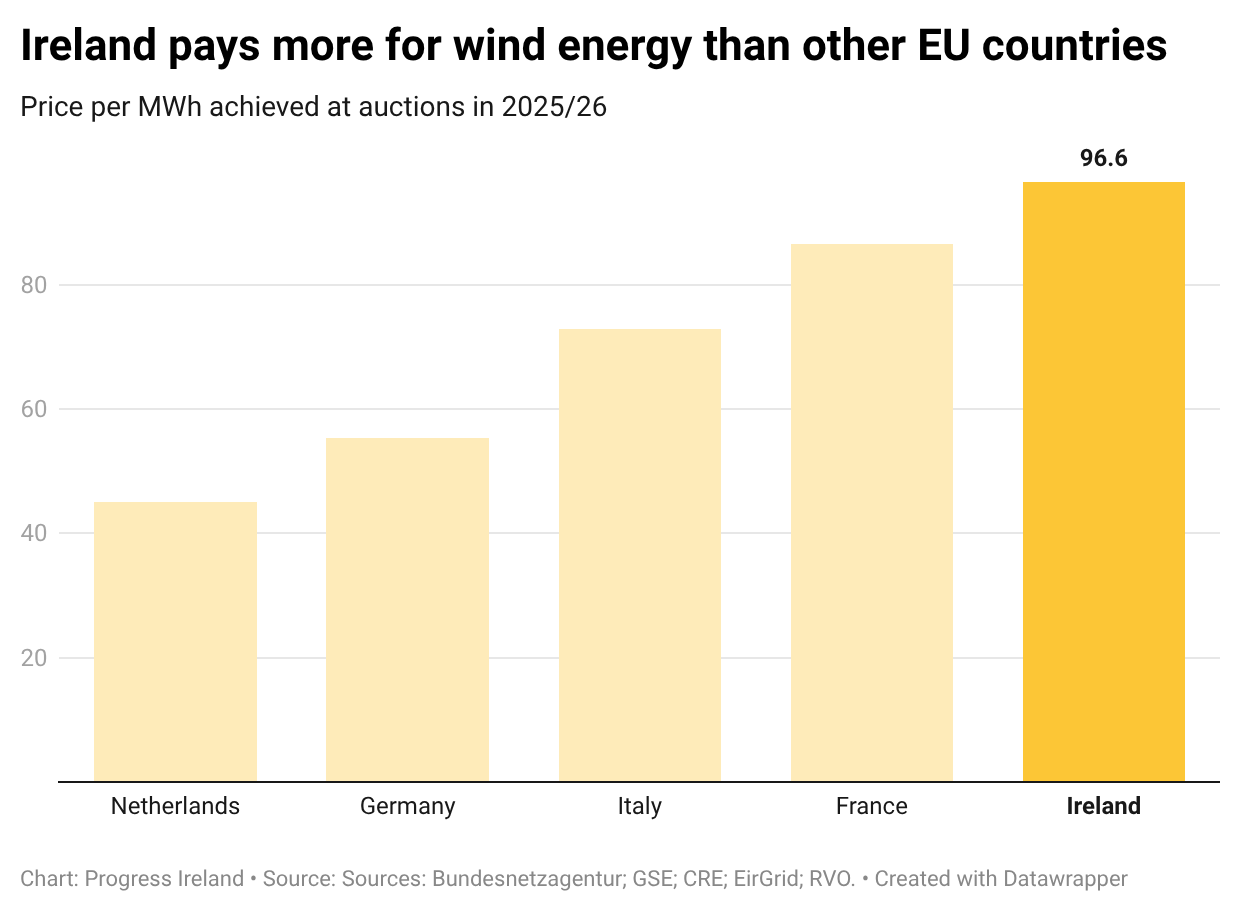

So it’s not the case that people are assuming wind will reduce our prices forever and ignoring the fact that you still have to pay for the wind. The part that really does worry me is that the price at which we’re procuring renewable electricity is in and around €100 a megawatt hour, which is way higher than our peer countries. If you look at the renewable auctions in Spain, Portugal, Denmark, the Netherlands, they’re getting wind as cheap as €35 a megawatt hour, and we’re paying nearly €100 — despite the fact that our wind resource is so much better than all of those countries.

Seán Keyes: Why?

Muireann Lynch: It’s the usual that we’re all sick of talking about in Ireland — planning, our legal system, the fact that everything gets JR’d, the fact that it takes five years to build a wind project here whereas in another country it might take one year.

Seán Keyes: Could we have wind at €35 a megawatt hour?

Muireann Lynch: What I can say is that other countries have wind at €35 a megawatt hour, and they have a worse physical resource than we do. And if you speak to actual developers who operate in Ireland and in other European countries — and developers should be taken with a grain of salt — they all tell you that Ireland is an order of magnitude more expensive and more complex to build in than any other European country they’ve built in, including the UK, which is not exactly easy on these things either.

Seán Keyes: So what I’m hearing is: we’re under-investing in energy of all kinds — renewables, gas — and our planning and environmental law is making renewables less economical than they ought to be. What I worry about is that transmission systems in particular are the most wicked problem in terms of our environmental law.

Muireann Lynch: A hundred percent.

Seán Keyes: It sounds like there’s some hope there. If the benchmark is what can be delivered in other European countries – surely we can reach that? Plus gas infrastructure as your backup. That seems like a path forward to a better system — if not exactly abundant and ultra-cheap, then probably a lot better than what we have today.

Muireann Lynch: Oh, totally. Although — I don’t know. We’re very much hearing the line lately of “we need energy to be affordable; it’ll never be cheap, we just need it to be affordable.” So we’ve kind of let go [of that]. We’re saying, look, we need to manage expectations here. And in some ways geography is against us, geology is against us; there’s only so far you can go. But it’s also stuff like the planning system being against us, and we’re all just sick of trying to fight that battle. Maybe we have to just take what we get.

Economists and their methods

Seán Keyes: What’s distinctive about the way economists think about the electricity system?

Muireann Lynch: It’s really important to understand not just the economics of the individual technologies, or of the system you want to operate, but also the interactions of different strategic players who have different incentives. You have generation and supply companies that want to maximise their profits. And you have regulators and policymakers who have a whole load of goals.

One thing that’s really helpful to reflect on is the Tinbergen rule: that you should have one instrument per policy. That rule grew out of central banking, but it’s violated an awful lot in the energy space. The job of the policymaker or regulator should be to have a reliable system. It’s their job, first, to define what they mean by reliable, and then to make sure the system meets that reliability standard. And they should deliver it at least cost. Those are the minimum requirements.

Some policymakers explicitly have extra requirements on top of reliability such as distributional concerns or supporting industry. Either way, you have a whole load of players with different incentives. They’re going to reach an equilibrium, and you want that equilibrium to be a good one. You cannot determine whether the equilibrium reached is good, or how to reach a good one, without an economic toolkit. That’s what economists bring to the table.

Seán Keyes: I read an economist analysing the Hormuz energy shortage. He said that a lot of technical people were focused on the shortages. They were calculating and extrapolating how the flows would cascade through the rest of the system. And by those calculations: it looked like there was going to be catastrophe. Whereas he, as an economist, trusted that markets and prices would adjust. He thought the outcome wouldn’t be as severe as the extrapolators thought. And in the event, he was proven right. Is there something to that? Why do economists and engineers sometimes come to different conclusions?

Muireann Lynch: I wouldn’t say so. No matter who you are, you’re using data and mathematical techniques to solve a problem. The question is what your assumptions are going in — what you’re assuming is a variable and what’s a parameter. It’s not so much about having faith in an equilibrium. It is a fact that we will reach an equilibrium, and the question is what that equilibrium will look like. To answer that, you have to ask: what are the moving parts going into this mathematical problem?

Now, some people ignore certain moving parts. For example, the fact that prices adjust, or that players respond to changes in prices, but also to physical realities. If you ignore those interactions, like assuming that demand will not adjust as prices go very high, you’ll reach a catastrophic solution. Whereas if you endogenise those responses to the surprises, you’ll reach a different solution, and it won’t necessarily be catastrophic.4

Seán Keyes: So is it the case that economists take greater pains to incorporate the adjustments that the suppliers and users of electricity will make to their behaviour in response to changes in prices?

Muireann Lynch: I’d endorse that. I’d just describe it as more of a tendency — there’s nothing stopping anyone saying “this is a variable, not a parameter.” But one of the things economists are particularly good at is understanding the difference between the short run and the long run, because we have that quite well defined in our models. The short run is defined by at least one of the factors of production being fixed, so you can’t increase supply. As soon as you move into a world where you can increase supply, then by an economic definition you’re in the long run.

Short run and long run are used in general discourse without that strict definition, which is fine. But if you don’t have any control over the number of units you’re supplying, then the only thing you have to work with is the price level. The only thing you can do is shove prices up or down to get demand to adjust to meet the fixed supply.

In the long run, if you can play around with supply, then you’ve got that lever available too — supply and price can adjust together to meet an equilibrium with demand. Economists are particularly good at understanding and deploying those dynamics. In the short run we’re dealing with prices only — what’s going to happen — and then how that feeds through to changes in supply, which kick in in the longer run. People from other disciplines are less likely to grapple with those dynamics.

It’s not “okay, the price is now 40 per cent higher, therefore the following will definitely happen,” and they don’t think about what else might adjust in the coming months or years. Prices will adjust, demand will adjust, and these feedback loops will kick in. This stuff is complicated. I’m not claiming it’s easy to solve, and sometimes these first-order approximations are incredibly useful. But that’s where I draw the distinction: short-run versus long-run thinking, and understanding how things move at the margin versus how things shift in levels.

Seán Keyes: I’m now going to present a straw-man image of your profession. In which you blithely assume away important real-world constraints that stop the long-term equilibrium from arriving. That, in reality, there are all sorts of complex logistics and constraints to take into account before your models can equilibrate. Is there a grain of truth in that?

Muireann Lynch: Honestly, no. It’s not that I don’t think we make unrealistic assumptions — everybody makes unrealistic assumptions, because you have to, to get anything to solve. Think back to Leaving Cert physics, calculating the rate at which something falls, and you’re told to ignore air resistance. That’s an “unrealistic” assumption. We all know air resistance exists, we all know something falls slightly slower than in a vacuum, but it’s good enough for what you’re doing. So I’m not saying economists, or anyone, don’t make unrealistic simplifying assumptions all the time. We absolutely do. Where we get straw-manned a fair bit is the idea that we somehow think the unrealistic assumptions are actually true. I won’t say no economist has ever thought that — not in a million years. But if someone insists that a simplifying assumption is actually true, then they’re just stupid, and they’re being a bad fill-in-the-blank: if they’re an economist, they’re a bad economist; if they’re a statistician, they’re a bad statistician.

One of the frustrations for me is that we’re very often not given the space — not given a seat at the table — because it’s “oh, look at these unrealistic assumptions, how stupid are they?” The point is: please tell us where the constraints are, and we’ll model them. This is what we do all day long — we optimise under constraints all day long. And these aren’t even “economic” models; they’re optimisation or operations-research models, used in all sorts of disciplines. There’s nothing magic about it — no one discipline owns these methodologies. What I’d say to my colleagues in all disciplines is: if you think an assumption is unrealistic, there’s a good chance I know it’s unrealistic and I’ve made allowances for it. There’s a good chance there are other assumptions I’ve made that I don’t even know I’ve made — please draw them to my attention and I’ll get them into my model. But if you come into it assuming that anyone who doesn’t explicitly model everything you personally think is important just thinks those things don’t matter, then you can never get off the ground.

Let me give you an example. A lot of power-system operation models go into huge detail modelling the stochasticity of electricity demand and supply — “we need thirty years of data on plant outages, thirty years of data on wind speeds and solar irradiance, to build a comprehensive model that properly accounts for all the variability, so we have a realistic representation in a stochastic framework”. And then they’ll run it under one gas-price assumption.5

It’s super important to get all those supply-demand uncertainties in there — and I also think it’s important to get fuel-price uncertainty in there. Never once in my life has an engineer turned around and said, “what are you talking about, fuel-price uncertainty is irrelevant.” Never. They’ve either said, “oh, good point — how would you model fuel-price uncertainty?” or “I understand where you’re coming from; in this particular model it’s particularly difficult to do, but what we intend to do is sensitivities around high and low fuel prices.” It would be super unhelpful of me to throw out stochastic operations-research modelling simply because those particular modellers happened not to model fuel-price uncertainty, and for me to decide therefore that they’re stupid and think the gas price never moves, when obviously they know it does.

A peaking power plant or “peaker” is a generator that runs only during periods of peak electricity demand or when other supply falls short, rather than continuously. In Ireland these are typically gas-fired, hence the contrast here with the company’s otherwise renewable portfolio.

A T-4 capacity auction is a mechanism for ensuring enough power-generation capacity exists to meet future demand. Rather than paying for electricity itself, the system pays generators to commit to being available to produce power when it’s needed. “T-4” means the auction is held four years ahead of the year the capacity is required, giving developers time to build new plants. In Ireland this runs through the all-island Single Electricity Market.

Muireann is referring to the target of 80 per cent renewables in the Climate Action Plan

Endogenise means to include something as a variable inside your model, as opposed to holding it fixed. In this case, it means accounting for how markets and people will react to unexpected events such as the closure of the Strait of Hormuz, rather than assuming they won’t.

Stochasticity refers to randomness in a system. A stochastic model accounts for the fact that real-world quantities like demand, wind speeds, plant failures can fluctuate unpredictably, and represents them as probability distributions rather than fixed values.

Last updated: